Kickstart Your Crypto Exchange Licensed in Bulgaria

07/10/2023

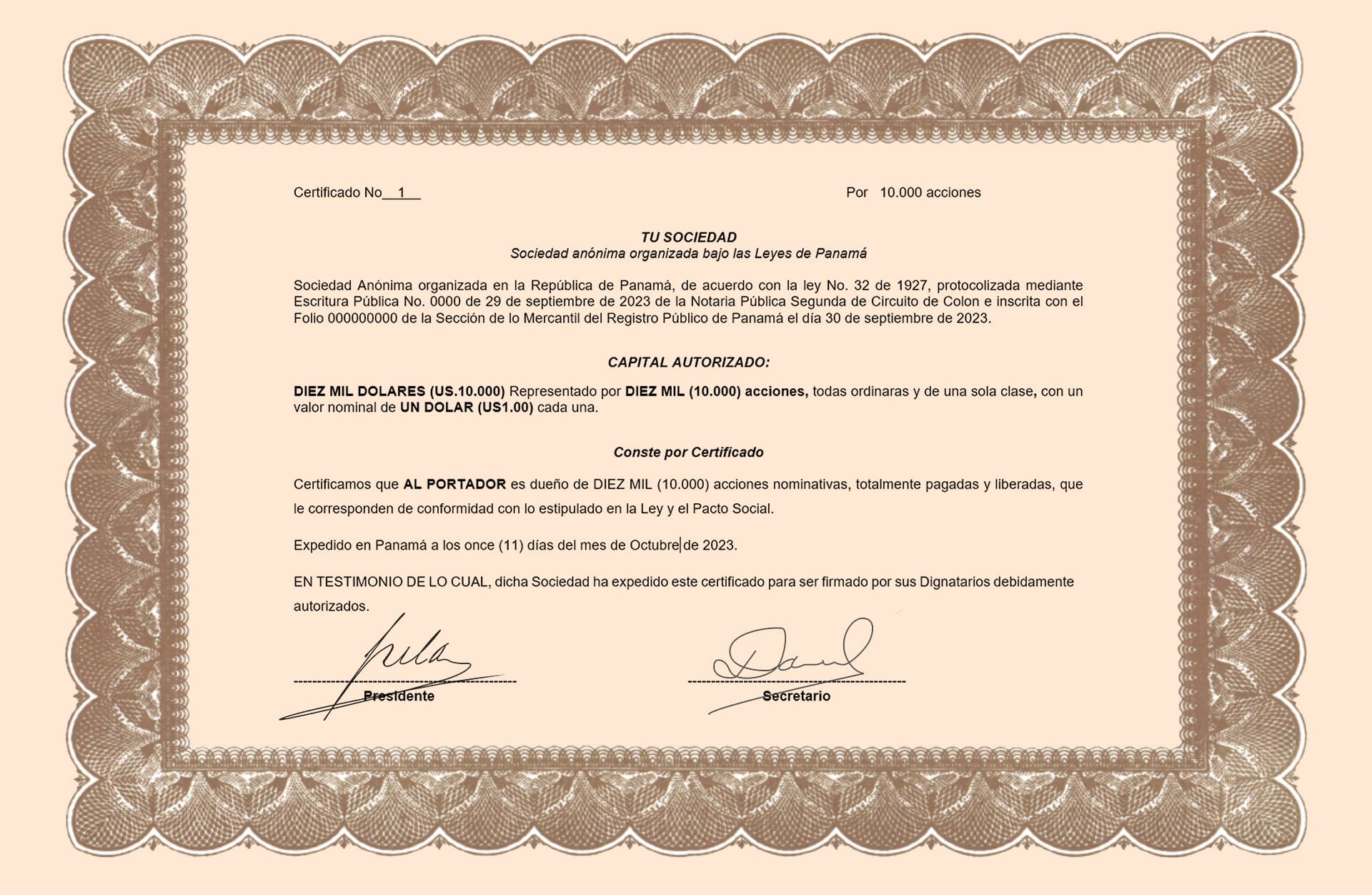

How does the custody of bearer shares work in Panama?

25/10/2023

Fiscal Residency vs Banking Residency: although they may seem similar, they have distinct functions and meanings, which deserve a thorough understanding so one must distinguish.

Tax residency concerns tax law and indicates the country in which a person is liable to pay taxes. It is usually based on the principle that if a person lives in a country for at least 183 days a year, that country becomes his or her tax residence. This means that the individual will have an obligation to declare his or her income and, consequently, to pay taxes in that country. It is worth noting that it doesn’t matter whether your business is in Europe or in a country outside Europe: if you have property or assets that generate income, you will have to declare that income.

However, what if a person owns property or assets in more than one country? Well, there may be situations where you have tax residence in more than one country. However, it is generally not advantageous to have tax residence in high-tax countries. For example, if a person has real estate in Italy that generates income, he will have to declare that income in Italy, regardless of his tax residence in another country.

Bank residency, on the other hand, relates to banking. When you open an account at a bank or other type of financial institution, they might ask you where you are tax resident. You might respond by saying you are resident in a country, such as Panama, but unless you have actually lived there for the aforementioned 183 days, you will not get the tax residency certificate required by some banks.

So what is the real difference? While tax residency is closely related to where you pay taxes, banking residency is more a matter of where you have domicile and established banking relationships. For example, you could have a banking residency in Panama (based on your official residence there) and use it to open bank accounts, even though you do not meet the requirements for a tax residency.

A significant advantage of bank residency is that it can provide some confidentiality. If you open a bank account in Panama and claim to be a tax resident there, the bank may not share your information with other countries. However, this may vary depending on intergovernmental agreements between countries and banking policies.

In summary, while both concepts are about “residency,” one focuses on taxes and the other on banking relationships.

As the world becomes increasingly globalized, it is critical to understand the distinctions between these two concepts and plan your business accordingly, especially if you intend to live, work, or invest in different countries.

In today’s context of economic globalization and digital interconnectedness, understanding the difference between taxes and banking residency is even more crucial. But why? Because what was once reserved for entrepreneurs, international investors and big fortunes now increasingly affects ordinary people working remotely, digital freelancers or anyone who wants to diversify their assets across national borders.

The growing popularity of remote work and the digitization of professions have made it easier than ever to live in one country and work for a company in another. This scenario can have tax and banking implications.

Imagine living in Spain, for example, and working for a U.S. company.

Where will you pay your taxes? Where will you have your main account? These are just a few of the dilemmas that can arise and underscore the importance of understanding the difference between the two concepts.

Another aspect to consider is the growing trend toward diversification of investments. Whereas investors once tended to invest in their own country, today they look for opportunities around the world. Someone might invest in real estate in Portugal, stocks in Hong Kong, and bonds in Australia. This geographic diversification poses new challenges in terms of tax and banking residency. Where is it best to open a bank account? In which country should certain income be declared?

Then there is the issue of asset protection. In a world where information can easily cross borders, confidentiality and protection of one’s assets are becoming increasingly important. This is where bank residency can come into play, offering an additional layer of privacy, depending on the jurisdiction.

But, as always, in addition to doing your own research you need to consult with subject matter experts, as laws and regulations change and what is valid today may not be valid tomorrow.

A brief telephone consultation on your particular case can help you make no mistake.

{kind=link}

{kind=link}

{kind=link}